THE AI PARADOX | PART III REPRISE: Locus of Control

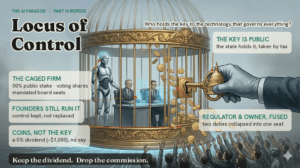

Bernie Sanders just gave Part III’s governance question a concrete answer: move control to the state. It is the mirror image of the White House framework’s answer. The real fight is over where control of AI should sit. This series has built a single argument across three parts. Part I asked whether a consumer economy can withstand AI-driven productivity gains. Part II reframed the risk as concentration rather than collapse, a modern Gilded Age in which productivity decouples from purchasing power as AI’s gains flow to whoever owns the compute, the models, and the data. Part III turned to governance and asked the question the first two demanded: who governs the technology that governs everything? The White House answered in March by declining to. Four pages, no regulator, no liability standard, no federal floor. Governance by abdication. This week the opposite answer arrived. On June 18, Senator Bernie Sanders introduced the American AI Sovereign Wealth Fund Act. It would have the public take a 50% ownership stake in the largest AI companies in the country, through a one-time tax paid not in cash but in stock. Where the framework governs by stepping back, the Sanders bill governs by stepping all the way in. Two answers to the same question, at opposite ends of the spectrum. Neither is the answer this argument has been building toward. But the gap between them is where the real fight now lives, and the Sanders bill is the more revealing of the two, because of who is standing near it. What Sanders actually proposed Strip away the framing and the mechanism is specific. A one-time 50% tax on the stock of any company with $200 million or more in annual receipts from AI activities. The stock goes into a federal sovereign wealth fund, estimated at $7 trillion at current valuations. A 5% annual dividend flows back out, roughly $1,000 per person to start. The proposed fund is to be run by an Independent Commission for Democratic AI: seven members nominated by the President and confirmed by the Senate from a bipartisan list, no more than four from one party. The commission votes the fund’s shares and seats representatives on each company’s board, with a mandate to block decisions it deems harmful to the public. The bill also requires structural separation: any company running both AI and non-AI businesses must stand its AI operation up as a separate entity, so the public stake lands only on the AI side. And it bars the fund from being used to bail out an AI company. It is not likely to pass a Republican-controlled Congress, and the bill is, for now, a marker. But markers matter, because of where the rest of the field already is. The public stake is no longer a fringe idea Here is the part that changes the story. The idea that the public should hold a direct stake in AI’s upside is no longer confined to one side of the left-right divide. Sam Altman has argued for a public vehicle to distribute AI’s gains broadly. Dario Amodei has written that taxes on AI companies could fund a universal basic income. Trump floated the government taking a position in AI developers and, in February, ordered Treasury and Commerce to draw up a sovereign wealth fund plan. So the disagreement is not whether the public should share in AI-generated wealth. On that, a socialist senator, two frontier-lab CEOs, and a Republican president are, in their very different registers, converging. The disagreement is about the instrument, and the control that rides along with it. Sanders said as much himself, dismissing the softer versions as billionaires deciding to buy off the public on their own terms. The instrument itself is not new to this argument. A participation stake in AI’s upside, modeled on Alaska’s Permanent Fund, broadening who owns the economy rather than taxing winners to compensate losers, is exactly the kind of mechanism worth building. Sanders has picked up the sovereign wealth fund by name. The diagnosis is shared. What he has done is attach that instrument to a control mechanism pointed in the opposite direction. Concentration, moved rather than solved The line that matters is not left versus right, and the question is not whether public ownership counts as socialist overreach. Public ownership of AI can empower citizens or it can centralize control, and that is the real divide. Participation broadens who owns the economy and leaves the upside in citizens’ hands. Transfer hands operational control to a government poorly equipped to drive the technology forward, and dulls the private incentives that produce it in the first place. Same instrument, opposite effects. The design choice is the whole question, not the ideological label on it. The Sanders bill is the transfer-and-control version. The dividend, the participation half, is real, and it is the part most worth keeping. It is bundled with a control half that does the one thing this whole argument has warned against. It concentrates power, just in a different place. The fair objection is that private concentration is already here, so why is a seven-member commission worse than six founders and a few index funds? It is not worse. It is additional. The bill does not trade private control for public control. It takes half the equity, leaves the founders running the companies, and adds a government control point on top. You now have both concentrations at once, plus a conflict the private version lacks: through the fund, the government becomes a 50% shareholder, voting the stock, in the firms it is supposed to regulate. This is the concern that has followed every state-controlled investment vehicle, and the funds that work tend to work by staying out of the way. Norway’s holds small, diversified stakes across thousands of companies and seeks operational control of none of them. Sanders proposes the reverse: concentrated voting power and board representation across the largest AI firms. The capture risk lives in that design choice, not in the public fund itself. Where the mechanism breaks Set the philosophy aside and judge the bill as a piece of engineering. Four problems surface, and the last goes straight to the governance question.

Bernie Sanders just gave Part III’s governance question a concrete answer: move control to the state. It is the mirror image of the White House framework’s answer. The real fight is over where control of AI should sit. This series has built a single argument across three parts. Part I asked whether a consumer economy can withstand AI-driven productivity gains. Part II reframed the risk as concentration rather than collapse, a modern Gilded Age in which productivity decouples from purchasing power as AI’s gains flow to whoever owns the compute, the models, and the data. Part III turned to governance and asked the question the first two demanded: who governs the technology that governs everything? The White House answered in March by declining to. Four pages, no regulator, no liability standard, no federal floor. Governance by abdication. This week the opposite answer arrived. On June 18, Senator Bernie Sanders introduced the American AI Sovereign Wealth Fund Act. It would have the public take a 50% ownership stake in the largest AI companies in the country, through a one-time tax paid not in cash but in stock. Where the framework governs by stepping back, the Sanders bill governs by stepping all the way in. Two answers to the same question, at opposite ends of the spectrum. Neither is the answer this argument has been building toward. But the gap between them is where the real fight now lives, and the Sanders bill is the more revealing of the two, because of who is standing near it. What Sanders actually proposed Strip away the framing and the mechanism is specific. A one-time 50% tax on the stock of any company with $200 million or more in annual receipts from AI activities. The stock goes into a federal sovereign wealth fund, estimated at $7 trillion at current valuations. A 5% annual dividend flows back out, roughly $1,000 per person to start. The proposed fund is to be run by an Independent Commission for Democratic AI: seven members nominated by the President and confirmed by the Senate from a bipartisan list, no more than four from one party. The commission votes the fund’s shares and seats representatives on each company’s board, with a mandate to block decisions it deems harmful to the public. The bill also requires structural separation: any company running both AI and non-AI businesses must stand its AI operation up as a separate entity, so the public stake lands only on the AI side. And it bars the fund from being used to bail out an AI company. It is not likely to pass a Republican-controlled Congress, and the bill is, for now, a marker. But markers matter, because of where the rest of the field already is. The public stake is no longer a fringe idea Here is the part that changes the story. The idea that the public should hold a direct stake in AI’s upside is no longer confined to one side of the left-right divide. Sam Altman has argued for a public vehicle to distribute AI’s gains broadly. Dario Amodei has written that taxes on AI companies could fund a universal basic income. Trump floated the government taking a position in AI developers and, in February, ordered Treasury and Commerce to draw up a sovereign wealth fund plan. So the disagreement is not whether the public should share in AI-generated wealth. On that, a socialist senator, two frontier-lab CEOs, and a Republican president are, in their very different registers, converging. The disagreement is about the instrument, and the control that rides along with it. Sanders said as much himself, dismissing the softer versions as billionaires deciding to buy off the public on their own terms. The instrument itself is not new to this argument. A participation stake in AI’s upside, modeled on Alaska’s Permanent Fund, broadening who owns the economy rather than taxing winners to compensate losers, is exactly the kind of mechanism worth building. Sanders has picked up the sovereign wealth fund by name. The diagnosis is shared. What he has done is attach that instrument to a control mechanism pointed in the opposite direction. Concentration, moved rather than solved The line that matters is not left versus right, and the question is not whether public ownership counts as socialist overreach. Public ownership of AI can empower citizens or it can centralize control, and that is the real divide. Participation broadens who owns the economy and leaves the upside in citizens’ hands. Transfer hands operational control to a government poorly equipped to drive the technology forward, and dulls the private incentives that produce it in the first place. Same instrument, opposite effects. The design choice is the whole question, not the ideological label on it. The Sanders bill is the transfer-and-control version. The dividend, the participation half, is real, and it is the part most worth keeping. It is bundled with a control half that does the one thing this whole argument has warned against. It concentrates power, just in a different place. The fair objection is that private concentration is already here, so why is a seven-member commission worse than six founders and a few index funds? It is not worse. It is additional. The bill does not trade private control for public control. It takes half the equity, leaves the founders running the companies, and adds a government control point on top. You now have both concentrations at once, plus a conflict the private version lacks: through the fund, the government becomes a 50% shareholder, voting the stock, in the firms it is supposed to regulate. This is the concern that has followed every state-controlled investment vehicle, and the funds that work tend to work by staying out of the way. Norway’s holds small, diversified stakes across thousands of companies and seeks operational control of none of them. Sanders proposes the reverse: concentrated voting power and board representation across the largest AI firms. The capture risk lives in that design choice, not in the public fund itself. Where the mechanism breaks Set the philosophy aside and judge the bill as a piece of engineering. Four problems surface, and the last goes straight to the governance question.

- The valuation math may undercut its own headline. The $7 trillion is priced off today’s valuations. A forced transfer of half a company’s equity, with public-interest directors attached, is the kind of event most analysts would expect markets to reprice for. If they do, even a moderate repricing pulls the fund below its advertised size. The bill itself concedes the direction, specifying that if these companies lose value, the loss falls on the companies, not the government.

- Capital formation bends around it. If crossing a revenue line, or simply having the wrong product mix, costs you half your equity, the rational response is to invest less, incorporate elsewhere, or structure to stay under the line. A policy meant to capture AI’s wealth can shrink it instead.

- The competitiveness problem is unilateral. The United States imposing this alone, while China, the United Kingdom, and the Gulf states do not, is a standing invitation for capital and incorporation to move. Frontier AI leadership is hard to regain once it leaves.

- The mandate fuses regulator and director. A corporate director owes a duty to the company’s shareholders. A regulator owes a duty to the public. The bill seats government directors on the board and orders them to serve the public interest even against the shareholders they sit for, with those decisions shielded from challenge. That does not add oversight to the firm. It collapses two duties built to stay separate into one seat, and moves the conflict between them inside the boardroom.

None of these is individually fatal to American AI leadership. Together, they break this design, not the goal behind it. The design is the whole game The deeper lesson from the governance argument is not about any single framework. It is that design determines outcome, and that the choice between regulate and innovate is a false binary hiding a far richer design space. The Haddon insight applies here too. You do not solve a systemic problem by picking a slogan. You solve it by engineering for how the system actually fails, and designing safeguards for each way it can fail. Seen that way, the Sanders bill and the White House framework are not opposites. They are two ways of getting the design wrong. One declines to provide any navigation. The other grabs the wheel by buying the car. Both leave power concentrated, only in different hands. That points to the confusion at the center of the bill. Sharing in AI’s wealth and governing AI’s risks are two different jobs. One is fiscal: who gets a cut of the gains. The other is regulatory: what the technology may do, who it can harm, how concentrated it can get. Both are necessary, and they pull against each other. An owner wants the asset to appreciate. A regulator has to be willing to cut its value when the public requires it. The bill hands both jobs to one commission, which is why its mandate lists financial solvency and fair competition in the same breath. You cannot maximize a firm’s value and police it with the same hand. The version worth arguing for separates the two jobs the bill fuses. For the fiscal one, a public claim on AI’s gains can be funded the way public wealth usually is: through taxation, through royalty structures on the public data and public research AI is built on, or through broad-based trusts that hold non-voting stakes. Each gives the public real cash flows from AI without the government voting the shares of the firms it also regulates. For the regulatory one, the foundation already exists but needs adapting: a federal floor with real obligations, antitrust aimed at the compute and infrastructure layer where concentration actually compounds, and mandatory incident reporting that surfaces systemic harm before it hardens. Rules that bind every AI firm, not a controlling stake in a chosen few. Keep the dividend. Regulate by rule. Drop the commission. The most useful thing about this week is not the bill’s odds, which are poor. It is the signal. When figures this far apart are all reaching for some version of a public stake, the question of whether the public should share in AI’s wealth has moved into the mainstream. The harder question, how to govern the technology itself, is still open. Both are design problems, and conflating them is how we end up getting both wrong. Four questions worth holding onto as this debate accelerates: If the public is going to share in AI’s wealth, does that require owning voting control, or only owning the upside? Those are separable, and conflating them is what turns a good objective into bad policy. Can a public fund hold equity in the largest AI firms without turning into a political instrument? The funds that manage it stay diversified and passive. A commission built to vote the shares and take board seats is the opposite of that. And if the line around an AI company is this blurry, who lands inside the gilded cage this bill is trying to build, and who quietly steps outside it? And if AI needs both a fairer share of its gains and real limits on its risks, should one institution be trusted to do both, or is the safer design to keep those two jobs apart? Part I: Can the Consumer Economy Withstand Widespread Productivity Gains? Part II: The Risk Isn’t Collapse. It’s Concentration. Part III: Who Governs the Technology That Governs Everything?